Wat Street

At Wat Street, I'm working on a market regime detection system that models the market as distinct behavioral states instead of just "up" or "down."

The goal is to avoid using one trading model for every environment. We detect the current regime first, then use that signal to route capital toward strategies that fit the conditions. That matters because market behavior changes over time, and models trained in one regime can fail when volatility and correlations shift.

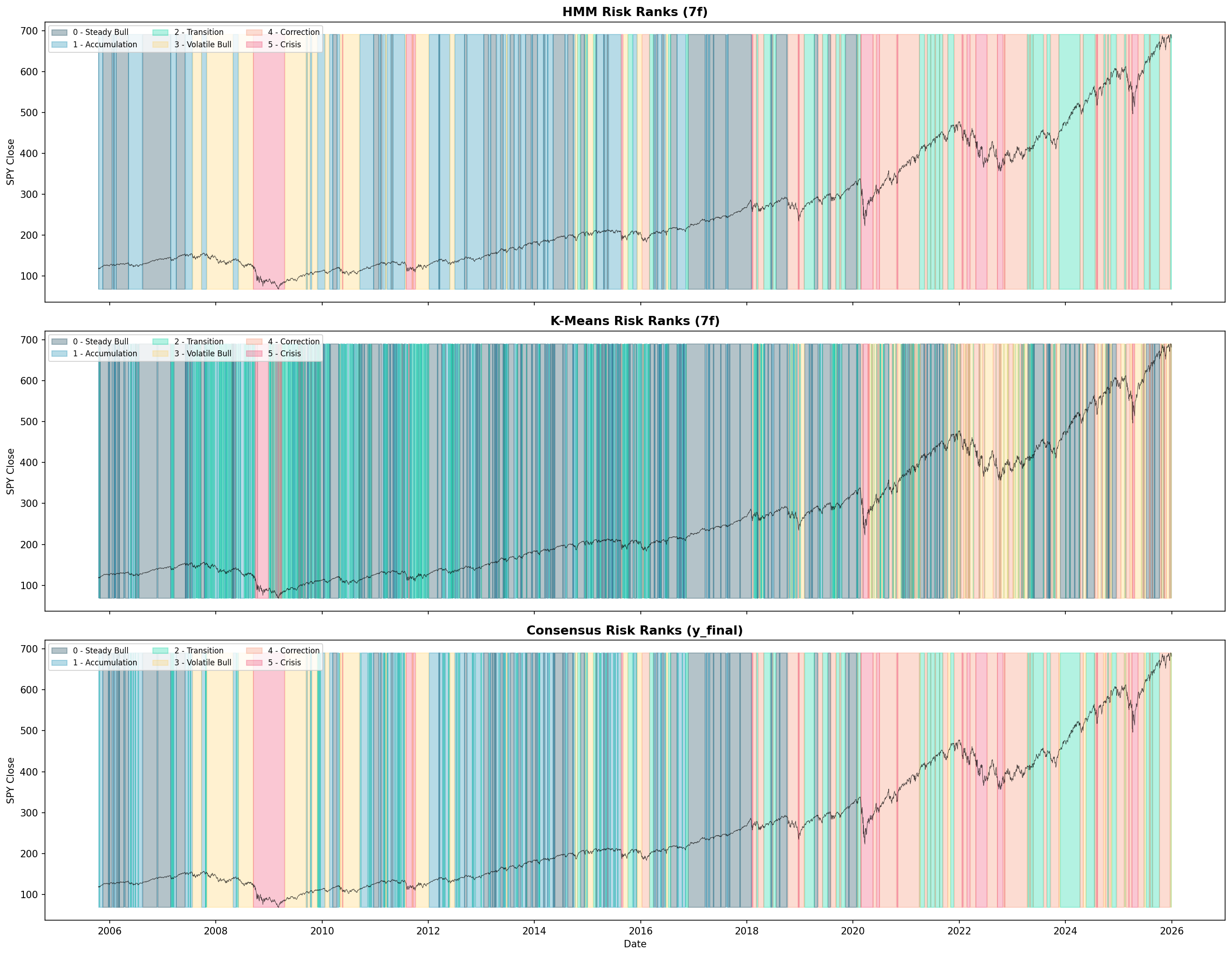

My work has focused on the labeling and forecasting pipeline: building the k-means clustering approach, improving agreement across labeling methods, creating the final labeled dataset with a pessimistic pivot rule (favoring the riskier state when models disagree), and training/optimizing a Temporal Convolutional Network (TCN) to predict regime transitions ahead of time.

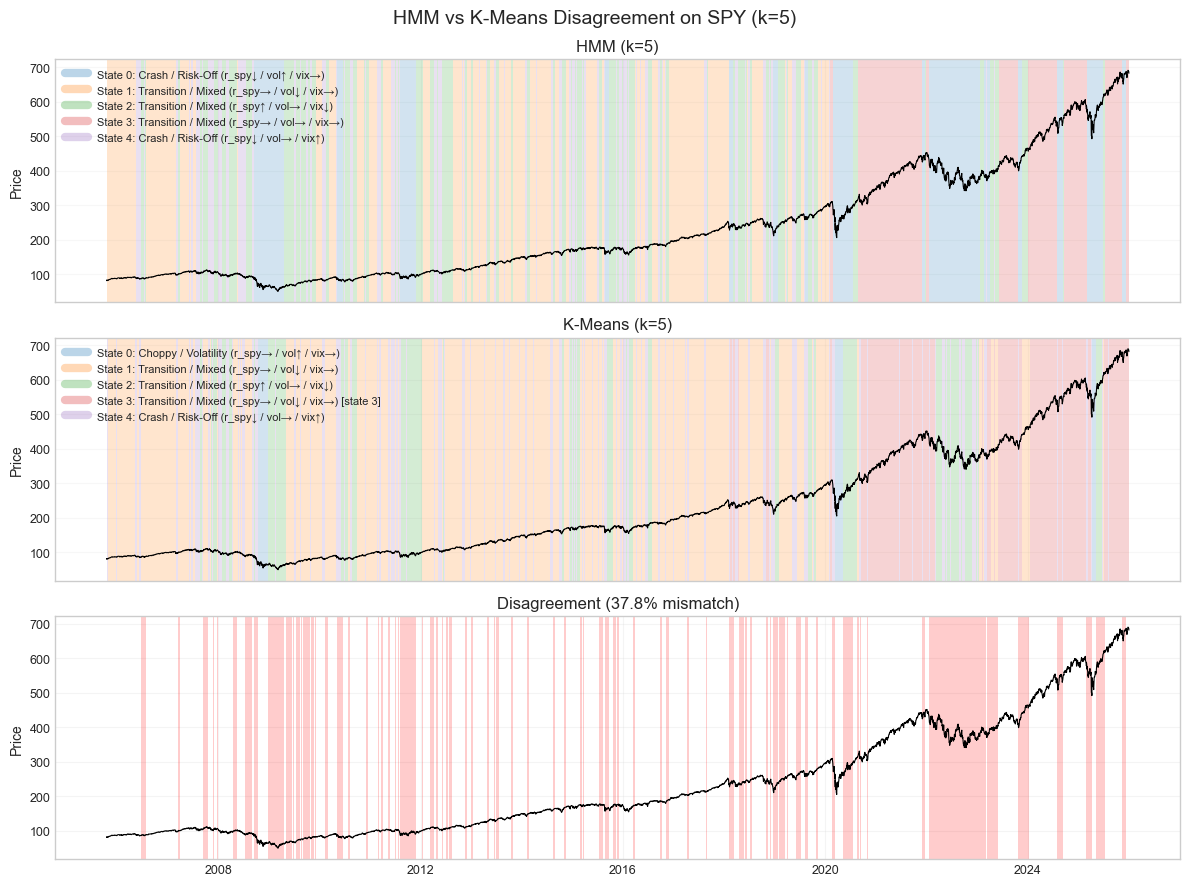

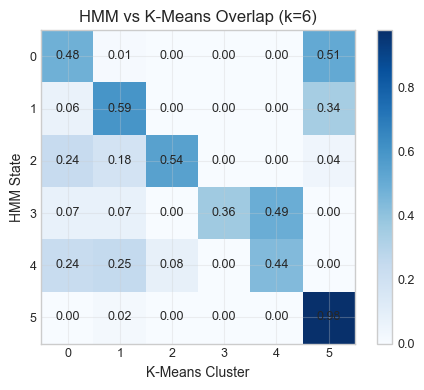

A big part of the work is making the labels trustworthy before using them for prediction. We compare unsupervised methods (Gaussian HMMs and k-means), check where they agree historically, and resolve the remaining conflicts with a risk-aware tie-break. We pushed agreement to about 81%, which gives us a much cleaner training signal than treating the labels as arbitrary clusters.

From there, the TCN is trained on the labeled sequences to forecast regime transitions. The target is not exact price prediction. It is to predict how the market is likely to behave next, early enough to switch strategies before the environment changes.